bestdesigns via Getty Images

One of the most under-appreciated aspects of the climate change problem is the so-called "fat tail" of risk. In short, the likelihood of very large impacts is greater than we would expect under typical statistical assumptions.

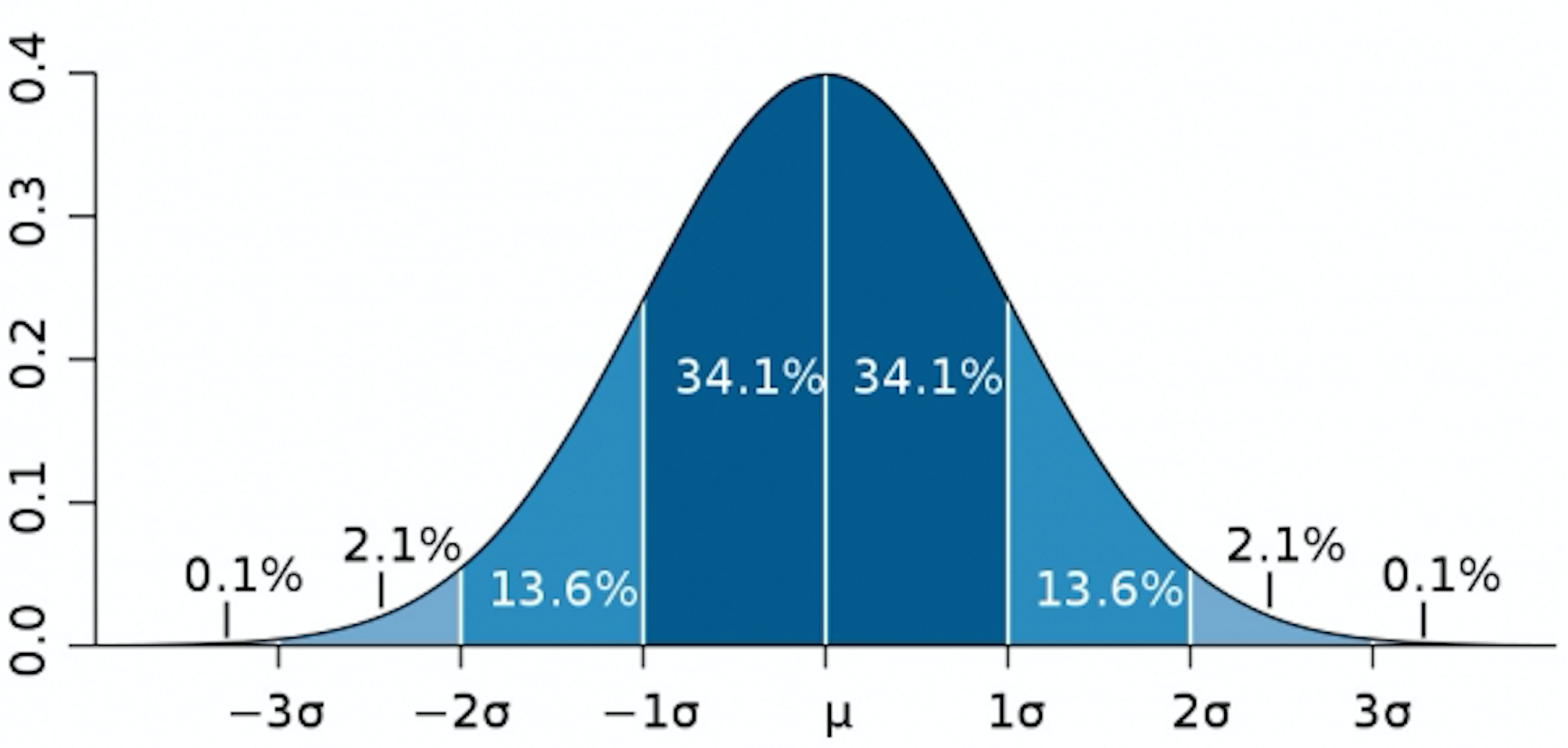

We are used to thinking about likelihoods and probabilities in terms of the familiar "normal" distribution -- otherwise known as the "bell curve." It looks like this:

Roughly 68 percent of the area falls within the region bounded by 1 standard deviation below (-1 sigma) and above (+1 sigma) the "mean" or "average", and a substantially greater 96% of the area falls between two standard deviations below (-2 sigma) and above (+2 sigma) the mean. So given this statistical distribution, we would expect values to fall above the +2 sigma (two standard deviation) limit only about 2% of the time. Call that the positive "tail" of the distribution.

There are many phenomena that follow a normal distribution, from the heights of adult men in the U.S. to the day-to-day fluctuations in summer temperature in New York City. But the predicted warming due to increased greenhouse gas concentrations isn't one of them.

Global warming instead displays what we call a "heavy-tailed" or "fat-tailed" distribution. There is more area under the far right extreme of the curve than we would expect for a normal distribution, a greater likelihood of warming that is well in excess of the average amount of warming predicted by climate models.

An important new book Climate Shock: The Economic Consequences of a Hotter Planet by Environmental Defense Fund senior economist Gernot Wagner and Harvard economist Martin Weitzman, explores the deep implications this has for the debate over climate policy.

Here's the blurb I wrote for the book (a shortened version of which appears on the back cover):

Think climate change is a low-priority problem? Something to put off while we deal with more immediate threats? Then Climate Shock will open your eyes. Leading economists Wagner and Weitzman explain, in simple, understandable terms, why we face an existential threat in human-caused climate change. The authors lay out the case for taking out a planetary insurance policy, without delay, in the form of market mechanisms aimed at keeping carbon emissions below dangerous levels.--Michael E. Mann, author of The Hockey Stick and the Climate Wars

The "insurance policy" analogy is appropriate here. We don't purchase fire insurance on our homes because our homes are likely to burn down. Far from it in fact: less than one-in-four homeowners are likely to ever experience a house fire. We purchase fire insurance because we understand that, even though such a catastrophic event is unlikely (less than 25 percent chance of happening), if it did happen, it would be catastrophic. So it is worth hedging against, by investing money now -- in the form of fire insurance.

Let us consider, in that context, the prospects for warming well in excess of what we might term "dangerous" (typically considered to be at least 2C or 3.6F warming of the planet). How likely, for example, are we to experience a catastrophic 6C = 11F warming of the globe, if we allow greenhouse gas concentrations to reach double their pre-industrial levels (something we're on course to do by the middle of this century given business-as-usual burning of fossil fuels)?

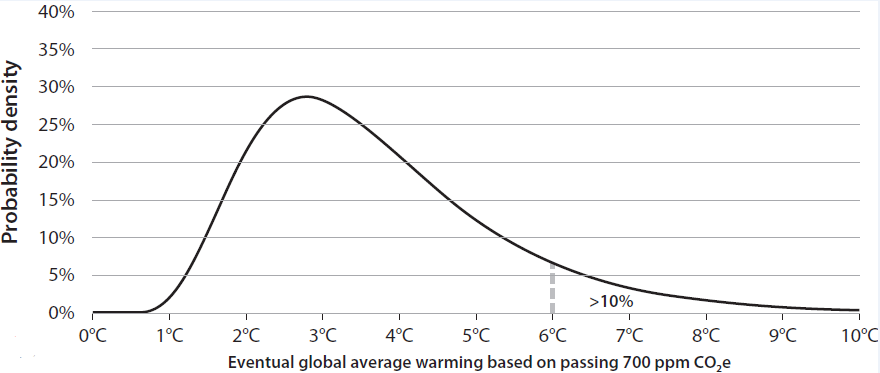

Well, the mean or average warming that is predicted by models in that scenario is about 3C, and the standard deviation about 1.5C. So the positive tail, defined as the +2 sigma limit, is about 6C of warming. As shown by Wagner & Weitzman (see figure below), the likelihood of exceeding that amount of warming isn't 2% as we would expect for a bell-curve distribution. It's closer to 10%!

An estimate of the likelihood of warming due to a doubling of greenhouse gas concentrations (Source: Wagner & Weitzman "Climate Shock" (via NPR)).

In fact, it's actually even worse than that when we consider the associated risk.

Risk is defined as the product of the likelihood and consequence of an outcome. We just saw that the likelihood of warming is described by a heavy-tailed distribution, with a higher likelihood of far-greater-than-average amounts of warming than we would expect given typical statistical assumptions. This is further compounded by the fact that the damages caused by climate change -- i.e. the consequence -- also increases dramatically with warming. That further increases the associated risk.

Risk is defined as the product of the likelihood and consequence of an outcome. We just saw that the likelihood of warming is described by a heavy-tailed distribution, with a higher likelihood of far-greater-than-average amounts of warming than we would expect given typical statistical assumptions. This is further compounded by the fact that the damages caused by climate change -- i.e. the consequence -- also increases dramatically with warming. That further increases the associated risk.

With additional warming comes the increased likelihood that we exceed certain "tipping points", like the melting of large parts of the Greenland and Antarctic ice sheet and the associated massive rise in sea level that would produce. Recent research suggests we may now have warmed the planet enough to insure at least 10 feet of sea level rise if not more. Some models suggest that that will take multiple centuries to happen. But maybe it will happen faster than the models predict.

Indeed, we have historically tended to underestimate the rate of climate change impacts. We reviewed the evidence in Dire Predictions: Understanding Climate Change, showing that many aspects of climate change -- e.g. the melting of Arctic sea ice and the ice sheets, and the rise in sea level -- have proceeded faster than the models had predicted on average. Uncertainty is not our friend when it comes to the prospects for dangerous climate change.

So we have to ask ourselves, do we feel lucky? If not, than we would perhaps be wise to purchase a planetary insurance policy in the form of policies to dramatically reduce our collective carbon emissions.

A recent article in Esquire by John H. Richardson explored the way various climate scientists (including myself) grapple with the complicated and indeed sometimes emotional task of communicating knowledge, uncertainty, and risk in a way that best informs the contentious debate over human-caused climate change and what to do about it.

OK. So now imagine my disappointment upon coming across an article that purports to embrace the thesis of Climate Shock -- in particular, the threat of the "fat tail" -- but in fact misunderstands it entirely -- and misrepresents, for good measure, theEsquire article and the scientists quoted in it -- including me.

The piece in question appeared at the tech-oriented website Quartz, authored by Allison Schrager, a self-described "economist, writer, and pension geek" with an interest in "how to hedge risk." The very title of the piece itself "Climate scientists undermine their own science by avoiding the best case scenario" is a falsehood, foreboding a fundamental misunderstanding of all of the principles explained thus far in this article.

In fairness, Schrager gets some things right. For example, she is correct when she states that:

[Wagner and Weitzman] use finance theory to argue the presence of risk is precisely why we need to limit carbon emissions sooner rather than later. In finance, risk poses a cost. You can pay to reduce it and often, the sooner you do, the cheaper it is to deal with the risk.

And she relevantly quotes Wagner on the the threat of the "heavy tail":

Wagner estimates there's a 10% chance of a catastrophic outcome. "That may be unlikely, but it's a huge freakin' problem," he told Quartz.

But it all then goes awry. In what has sadly become an all-too familiar pattern of blaming the scientists (yes -- this mess we've gotten ourselves into is all the fault of the scientists!), Schrager levels a number of cheap shots against climate researchers.

She accuses climate scientists, for example, of using "more forceful language" (horrors!) and of seeking to "underplay the uncertainty that still exists" (without even an iota of evidence to support that contention).

Then, in what frankly smacks of concern trolling, expresses her deep distress about what is "at stake":

Considering what's at stake, the extreme measures and playing up the stark predictions are understandable. But exaggerating the likelihood of extreme outcomes not only give deniers ammunition, it undermines convincing--even if not entirely certain--science.

Yes, those climate scientists are "exaggerating extreme outcomes" -- and that's what is fueling climate change denialism (something I happen to know a thing or two about) and undermining science!

OK -- and the evidence for this laundry list of accusations against climate researchers? A single quote mine of the Esquire piece. And the minee? Yes indeed -- your's truly.

Seeking to provide an example of how "climate scientists feel a need to go so extreme" she quotes the following passage in the Esquire article involving me:

As Mann sees it, scientists like [NASA/GISS scientist Gavin] Schmidt who choose to focus on the middle of the curve aren't really being scientific. Worse are pseudo-sympathizers like Bjorn Lomborg who always focus on the gentlest possibilities. Because we're supposed to hope for the best and prepare for the worst, and a real scientific response would also give serious weight to the dark side of the curve.

I've added the emphasis, because Schrager appears to have missed the words "focus" and "also" which are absolutely critical to a meaningful reading of that passage. The point being made there is that we shouldn't only consider the central tendencies (the mean). We need to ALSO consider the worst-case scenarios -- the FAT TAIL, to fully assess the associated risk. It is what Climate Shock is literally all about.

But Schrager continues with the straw man that she's constructed:

As a pension economist I understand the temptation to over-emphasize the worst case.

No. Let's be clear about this. Nobody here is arguing to "over-emphasize the worst case". Not me. Not anyone quoted in the Esquire article. All we're arguing is to not neglect the fat tail.

The straw man continues to the very end of the article, with Schrager concluding:

It's tempting to shout from the rooftops that this is a disaster waiting to happen, because the downside is so scary -- even if it will only impact our grandchildren. More so for climate change where the stakes are so much bigger. But that only gives skeptics room to question climate scientists' findings. If anything, the existence of uncertainty provides the best case for swift action because the solutions (cap-and-trade, investment in renewables) are relatively cheap compared to what they will be in the future if worst cases are realized.

Which means that she apparently didn't really get anything out of Climate Shock at all.

The actual reason uncertainty provides the "best case for swift action", as explained in excruciating detail in Climate Shock, is the FAT TAIL of risk emphasized by Wagner and Weitzman (and by me in the Esquire piece). The best reason for taking out a planetary insurance policy is the non-negligible likelihood of climate changes that are considerably greater, and risks that are more severe, that our average current predictions. That, in a sentence, is the thesis of Climate Shock.

There is need for a nuanced discussion of climate risk and solutions, and the challenges inherent in decision making in the face of uncertainty -- things I always stress in my commentaries and public speaking engagements about climate change.

But straw man constructions that caricature these nuanced matters and misrepresent the scientists and their efforts to inform this critical discussion, does absolutely nothing to advance that discussion. Indeed, it does quite a bit to harm it.

As we head into the all-important UN summit in Paris this December, which is perhaps our last chance for an international treaty that will avert dangerous and irreversible climate change, it is time for serious people and serious discussions, not straw men and distractions. We simply can't risk that.

Michael Mann is Distinguished Professor of Meteorology at Pennsylvania State University and author of The Hockey Stick and the Climate Wars: Dispatches from the Front Lines and the recently updated and expanded Dire Predictions: Understanding Climate Change.

{kind=link}

No comments:

Post a Comment